Thinking about buying a home in Florida—but not sure how the process works?

Since 2009, we’ve helped Florida homebuyers navigate the mortgage process in a way that’s clear, efficient, and designed to cut down the stress, delays, and uncertainty that often come with getting approved for a home loan.

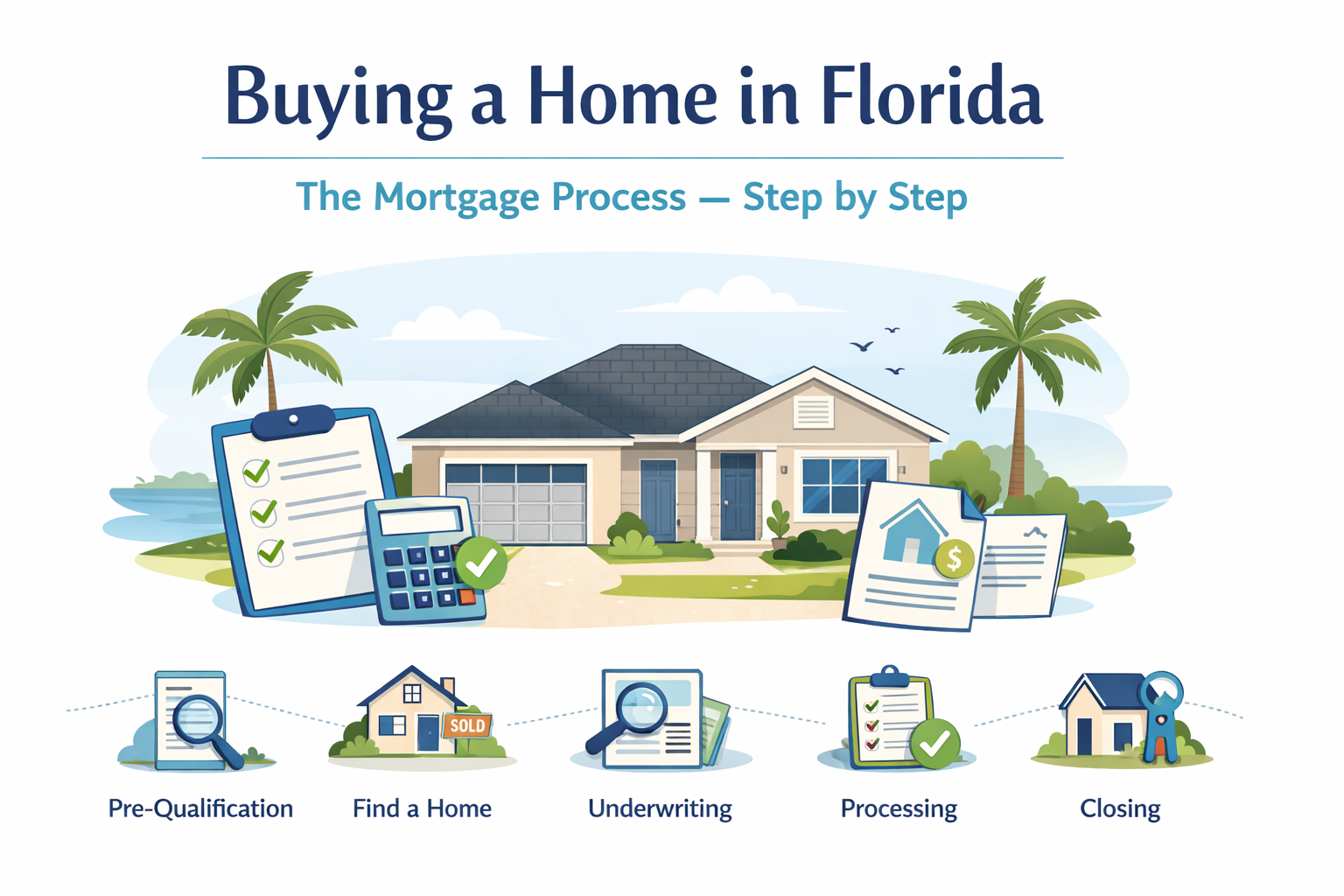

Below, we’re breaking our loan process down into five simple steps, so you can move forward with confidence.

Step 1: Pre-Qualification or Pre-Approval

A lot of buyers skip this step and jump straight into house hunting—but this is really where everything begins.

Getting pre-qualified or pre-approved before you start looking at homes shows sellers that you’re a serious buyer and ready to move forward. It also gives you a clear understanding of what you can comfortably afford, so you’re not falling in love with homes that end up being out of reach.

The best part? This step only takes a few minutes and is completely online.

When you complete this step, you’ll receive a pre-qualification or pre-approval letter you can present to sellers along with your offer. You’ll also get a clearer picture of your estimated monthly payment and how much cash to close you may need. It also gives you the chance to review loan options with your loan officer and talk through what makes the most sense for your goals.

You can get started by clicking here. Once you’re connected with a loan officer, complete your application, and we review your credit, we’ll provide a pre-qualification or pre-approval letter outlining what you qualify for.

Want a breakdown of the difference between a pre-qualification and a pre-approval? You can read more here.

Step 2: Find a Home

Now that you have a clear idea of your budget, it’s time to start your home search.

Having a clear budget helps makes the process feel much more manageable and keeps your search focused. This is also where working with a realtor can be incredibly helpful. They’ll guide you through showings, offers, and negotiations so you don’t feel like you’re figuring everything out on your own.

Take your time, explore your options, and find a place that truly feels like home.

Step 3: Underwriting

Once you’ve found a home, your offer is accepted, and you’re officially under contract, your loan moves into underwriting. An underwriter is the person who reviews all your financial details to make sure everything lines up —your income, credit, assets, even the property.

Then, the underwriter will issue a loan approval with conditions. Think of conditions as requirements to finalize the loan, so “you’re good to go, as long as…”

Step 4: Processing

In processing, you’ll be paired with a processor from our team to review any conditions from underwriting and work with you to clear those conditions.

This means gathering any additional documents or information needed to move things along. The goal is to make sure everything’s in order, acceptable, and ready for a smooth closing well ahead of your scheduled closing date.

Step 5: Clear to Close

Once all conditions are reviewed and approved, the underwriter issues a Clear to Close, also known as final approval.

Then, your file will be passed to our closing team, who will work with the title company to fine tune and balance all figures.

On closing day, you’ll sign the final paperwork, your loan will be funded, and just like that—you’re officially a homeowner.

If you ever have questions along the way, you’ll be supported by a team of local professionals who genuinely care about making sure you’re taken care of.